5 Steps to Budget Fixed and Variable Expenses

Five steps to categorize fixed vs variable costs, calculate monthly averages, match expenses to income, and track your budget.

Master your budget by balancing fixed and variable expenses. Fixed costs like rent stay consistent, while variable costs like groceries fluctuate. Understanding this distinction helps you control spending and plan better.

Key Takeaways:

- Step 1: Gather financial records (bank statements, receipts) to track spending accurately.

- Step 2: Sort expenses into fixed (e.g., rent, insurance) and variable (e.g., groceries, utilities) categories.

- Step 3: Calculate average monthly costs using 3–12 months of data for precision.

- Step 4: Compare expenses to income, adjust discretionary spending, and apply budgeting methods like the 50/30/20 rule.

- Step 5: Monitor your budget monthly, update for life changes, and refine spending habits.

By following these steps, you’ll reduce financial stress, avoid surprises, and align spending with your goals. Start today with a clear financial snapshot.

5 Steps to Budget Fixed and Variable Expenses Infographic

Fixed vs Variable Expenses: What They Are and How to Budget for Them

sbb-itb-ba81f5d

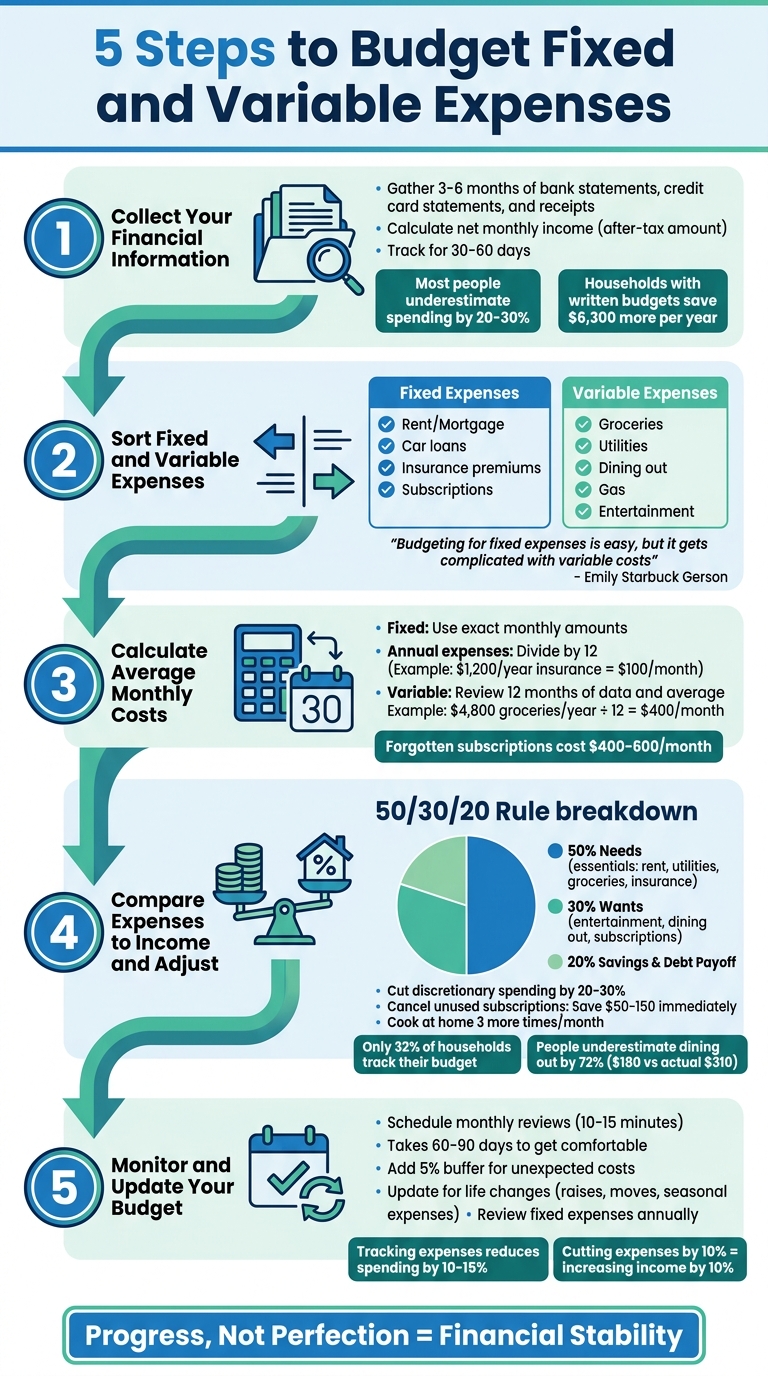

Step 1: Collect Your Financial Information

Start by gathering accurate data from your financial records. Did you know that most people underestimate their monthly spending by 20% to 30%?. This gap often leads to budgeting failures, so having a clear financial snapshot is key to managing both fixed and variable expenses effectively.

"Knowing the truth about where your money is going is the foundation of every good budget." – Every Dollar Grows

While this step requires some effort upfront, it’s worth it. Households that stick to a written budget save an average of $6,300 more per year compared to those without one. To get started, gather three to six months of bank statements, credit card statements, and receipts. This timeframe helps you capture your spending habits and account for irregular expenses that could throw off your budget.

Calculate Your Net Monthly Income

Your budget begins with net income - the amount actually deposited into your account after deductions like taxes, health insurance, and retirement contributions. Using your gross salary instead of net income can lead to overestimating how much you have available to spend.

If you’re paid regularly, check your most recent paystub for your net pay. For those with multiple income sources, add up all after-tax deposits. If your income varies month to month, you have two options: average the last six months of income for a more balanced view, or use your lowest-earning month as a conservative baseline to ensure you can always cover essentials.

Gather Financial Documents

Next, collect all necessary financial records and keep an eye out for unexpected charges. On the income side, this includes paystubs showing net pay, freelance invoices, 1099 tax forms, and any documentation for alimony or child support. For expenses, gather loan agreements, utility bills, and any other statements that detail your monthly costs.

Track every transaction for at least 30 to 60 days, including small cash purchases. Highlight forgotten subscriptions or duplicate services - they often account for $400 to $600 of "missing" money each month. Once you’ve got a complete picture of your finances, you’ll be ready to organize your fixed and variable expenses in Step 2.

Step 2: Sort Fixed and Variable Expenses

With your financial documents in hand, the next step is to organize your expenses into two main categories: fixed expenses and variable expenses.

Fixed expenses are the predictable, recurring costs that stay the same each month. These typically include rent or mortgage payments, car loans, insurance premiums, and subscriptions like gym memberships. On the other hand, variable expenses fluctuate depending on your choices and needs. Think groceries, utilities, dining out, gas, or unexpected car repairs.

"Budgeting for fixed expenses that remain the same each month is easy, but it gets more complicated once you factor in variable costs that are less predictable." – Emily Starbuck Gerson, Journalist, Experian

To make this distinction clearer, go through your financial statements from the last three to twelve months. This will help you spot patterns - what stays consistent and what varies. Fixed expenses often represent your biggest financial obligations, while variable expenses may offer more opportunities to adjust and save.

Keep in mind that both categories include essentials (like rent or food) and non-essentials (like entertainment or dining out). Sorting your expenses this way not only highlights areas where you can cut back but also sets the stage for calculating your average monthly costs in Step 3. Once everything is sorted, you’re ready to move forward!

Step 3: Calculate Average Monthly Costs

Now that your expenses are organized, it’s time to calculate your average monthly spending. This step ensures your budget is based on actual numbers, not guesses, which can lead to costly mistakes.

Fixed expenses are relatively simple to figure out, while variable expenses take a bit more effort. Both are critical for creating a budget that reflects your real financial habits. Let’s break these down further.

Track Fixed Expenses

Fixed expenses are the easiest to calculate because they stay consistent each month. Think of items like rent or mortgage payments, car loans, insurance premiums, gym memberships, and minimum payments on loans. These amounts don’t change, so you can pull the exact figures from your financial statements.

This stability provides a solid foundation for measuring and managing your variable costs.

That said, not all fixed costs are monthly. Some, like car registration fees, annual insurance premiums, or tax preparation services, are billed annually or quarterly. To handle these, total the annual cost and divide by 12 to find the monthly average. For example, if your car insurance is $1,200 per year, set aside $100 each month in a "sinking fund" to avoid scrambling when the bill arrives.

You should also count automated savings - whether for retirement, college funds, or emergency reserves - as fixed expenses. This ensures they’re treated as non-negotiable items in your budget.

Analyze Variable Expenses

Variable expenses are trickier since they change from month to month. Categories like groceries, dining out, utilities, gas, and entertainment require a deeper dive. To find a reliable average, review 12 months of spending. Add up the total for each category and divide by 12.

For example, if you spent $4,800 on groceries over the past year, your monthly average is $400. Looking at a full year of data ensures seasonal fluctuations - like higher heating costs in winter or increased travel during summer - are accounted for.

Breaking variable expenses into subcategories can also reveal where your money is really going. Instead of grouping everything under "food", separate groceries from dining out. This level of detail can uncover areas where you might be overspending. For instance, many people discover they’re paying for unused subscriptions, which can save them $50 to $150 right away once canceled.

Step 4: Compare Expenses to Income and Make Adjustments

Using the averages you calculated in Step 3, it’s time to see how your spending stacks up against your income. This step is where the reality of your financial habits becomes clear.

Start by summing up all your fixed and variable expenses. Then, subtract this total from your net income. If the result is positive, congratulations - you’re living within your means. If it’s negative or cutting it dangerously close to zero, you’ll need to make some changes. Interestingly, only 32% of American households actively track their monthly budget as of 2025. Yet, those who do manage to save an average of $6,300 more per year than those who don’t.

Find Overages and Cut Back

If your expenses outpace your income, start by trimming discretionary spending - your “Wants.” This includes things like dining out, streaming services, entertainment, and impulse buys. These are the easiest areas to adjust without affecting your essential needs.

Take some time to scan your bank statements for forgotten subscriptions - those “ghost” services you signed up for and no longer use. Canceling these could free up $50 to $150 almost immediately. A behavioral study revealed that participants estimated they spent $180 on dining out, but actual spending records showed $310 - a 72% gap. This kind of “spending blindness” is surprisingly common, especially with small, frequent purchases like coffee or snacks, which people tend to underestimate by 35-40%.

Instead of cutting entire categories, aim to reduce discretionary spending by 20-30%. For example, cooking at home just three more times a month instead of eating out can save a noticeable amount without feeling like a drastic lifestyle shift. Focus on making sustainable changes rather than extreme cutbacks, and then apply a structured budgeting method to keep things balanced.

Apply the 50/30/20 Rule

The 50/30/20 rule is a straightforward way to allocate your income: 50% for Needs (essentials like rent, utilities, groceries, and insurance), 30% for Wants (non-essentials like entertainment and dining out), and 20% for Savings and Debt Payoff. This approach helps you pinpoint any imbalances in your spending.

To use this method, divide each expense category by your net income to calculate its percentage. If your Needs are taking up 60% or more of your income, it might be time to reevaluate larger fixed costs, like housing or transportation, though these adjustments may take time. For those living in high-cost areas or aggressively paying off debt, you can tweak the rule to ratios like 60/20/20 or 50/20/30 to suit your situation.

The rule is flexible. For example, high earners making $150,000 or more might opt for a 40/20/40 split, allowing them to save 40% of their income. The most important takeaway? Always prioritize the 20% savings goal whenever possible. When money feels tight, start by trimming Wants rather than compromising your savings.

Step 5: Monitor and Update Your Budget

Once you've refined your budget in Step 4, the real challenge begins: keeping it on track through consistent monitoring and adjustments.

Creating a budget is just the first step - the real work lies in tracking and revising it regularly. Think of your budget as a dynamic tool, not a static document. By actively monitoring your spending, you can gain better control over your finances. In fact, studies suggest that tracking expenses alone can help reduce overall spending by 10–15%. On average, it takes about 60–90 days to get comfortable with managing a budget.

Schedule Monthly Reviews

Set aside a specific day each month - right after payday is ideal - to review your spending against your budget. Many people find that Sunday evenings work well for this task. Devote 10–15 minutes to reviewing your recent transactions, making adjustments to categories, and planning for upcoming expenses. These regular check-ins can help you spot overspending early. For instance, if you're approaching the limit in a discretionary category halfway through the month, you can make small adjustments to avoid going over budget.

At the end of each month, take a closer look at where you overspent. Instead of completely reworking your budget, tweak category limits for the next month. If one area consistently exceeds its limit while another has leftover funds, shift money between categories. You could also add a buffer category - around 5% of your total variable budget - to handle unexpected costs without throwing off your entire plan. These monthly reviews are essential for connecting your initial budget setup to long-term financial success.

Be prepared to adjust your plan regularly as changes occur in your spending habits or financial priorities.

Update for Life Changes

Whenever your financial situation shifts, update your budget immediately. This could mean receiving a raise, starting a job with a new pay schedule, or moving to a place with different living costs. Seasonal changes can also affect your budget. For example, heating bills may spike in winter, air conditioning can raise summer costs, and holiday or vacation expenses might require extra planning. Reviewing 6–12 months of past spending can help you anticipate these patterns and incorporate them into your budget.

It's also a good idea to reassess fixed expenses, like insurance, internet plans, and subscriptions, at least once a year - ideally before any contracts automatically renew. You may find opportunities to save. For irregular but predictable expenses, such as annual memberships, car registration fees, or holiday gifts, consider setting up sinking funds. Divide the total annual cost by 12 and save that amount each month. This approach can help you avoid financial surprises and keep your budget steady.

Conclusion

Managing fixed and variable expenses doesn’t have to be complicated. By following five essential steps - gathering your financial details, categorizing expenses, calculating monthly averages, comparing them to your income, and regularly keeping track - you can create a clear path toward financial stability. These steps help you establish a "floor" for your spending by focusing on fixed costs.

The key to long-term success is treating your budget as a flexible tool that evolves with your changing needs. As Chris Holmes, Finance Writer and Editor at Ramp, explains: "Budgeting works best when fixed costs are covered first and variable spending is actively monitored". This approach ensures that your essential expenses are prioritized while keeping discretionary spending under control. By treating your budget as a living document, you can adapt it to align with your goals and circumstances.

Small, steady changes can make a big difference. For example, trimming expenses by just 10% has the same impact on your bottom line as increasing your income by 10%. Whether you follow the 50/30/20 rule or another budgeting framework, committing to a quick monthly review - just 10–15 minutes - can help you stay aligned with your financial goals. Over time, this habit can pave the way for paying off debt, building an emergency fund, and accumulating long-term wealth.

Start with Step 1 today. Progress, not perfection, is what leads to lasting financial stability.

FAQs

What’s the easiest way to budget when my income changes every month?

The simplest way to create a budget with a fluctuating income is to start by calculating your average monthly income. Use past earnings - like bank statements or annual income totals - as a guide. This average gives you a solid foundation to plan your budget.

To manage the ups and downs, set up a flexible system. During months when your income is higher, save the extra money to cover expenses during lower-income months. This strategy can help you maintain financial stability, even when your income isn’t consistent.

How should I handle annual or irregular bills in a monthly budget?

To handle annual or irregular bills smoothly, set aside a portion of your income each month. Start by estimating the total yearly cost of these expenses, then divide that number by 12. Save this amount monthly to build a dedicated fund. This way, when those bills come due, you’ll have the money ready without throwing off your regular budget. Periodically review and adjust your savings to ensure you’re staying aligned with your goals.

How can I stop overspending on variable expenses like food and utilities?

To keep variable expenses in check, start by breaking down your spending into categories like groceries, dining out, and utilities. Set a budget for each category that feels realistic for your lifestyle. Make it a habit to track your expenses consistently, so you can monitor how close you are to your limits. It's also smart to include a small buffer for any surprise costs that might pop up. Finally, focus on mindful spending - pause to review purchases before making them, and consider using tools or apps to help you stay accountable to your budget.